The Bank of Japan (BOJ) has been practicing unconventional monetary easing for more than 2 decades. Under Haruhiko Kuroda’s 10-year governorship from March 2013 to April 2023, the BOJ became known as a bold practitioner of monetary easing (New York Times 2023), introducing quantitative and qualitative monetary easing (QQE) in 2013 and yield-curve control (YCC) in 2016.

The Bank of Japan (BOJ) has been practicing unconventional monetary easing for more than 2 decades. Under Haruhiko Kuroda’s 10-year governorship from March 2013 to April 2023, the BOJ became known as a bold practitioner of monetary easing (New York Times 2023), introducing quantitative and qualitative monetary easing (QQE) in 2013 and yield-curve control (YCC) in 2016.

Japan gradually moved away from deflation, and inflation has been above the 2% price stability target since April 2022. The contributing factors—of which commodity price factors as well as the depreciation of the yen are key—are external in nature and likely to dissipate. There is a risk that inflation may fall well below 2% again if the BOJ withdraws prematurely from its current policies. However, the likelihood of inflation returning to negative territory may be lower because of supply-side factors, such as labor shortages, rising production costs in the People’s Republic of China and the relocation of production to Japan and other countries, climate change, and the Russian invasion of Ukraine.

It is uncertain whether sustainable 2% inflation is achievable from higher domestic demand-driven wage growth in the rapidly progressing aging economy. The recent decade of aggressive monetary easing should also be understood from a longer-term perspective covering the 1980s and a series of unconventional monetary easing experiments, starting with the zero-interest rate policy adopted in 1999 (for details, see Kowalewski and Shirai (2023)).

BOJ’s substantial monetary easing stance since 2013

QQE consisted of a shift of the operational target from the short-term interest rate (overnight uncollateralized call rate) toward the monetary base. To achieve 2% inflation with a time horizon of about 2 years, the BOJ announced an annual increase in the monetary base in the range of ¥60 trillion–¥70 trillion. It focused on raising long-term inflation expectations to bring negative real interest rates. However, inflation expectations declined from 2014 due to a sharp decline in oil prices and the consumption tax, which led the BOJ to accelerate the pace of increase in the monetary base to about ¥80 trillion.

In 2016, the BOJ became the fifth major central bank to announce a negative interest rate policy, exerting strong downward pressure on long-term interest rates (Shirai 2018). Due to a substantial concentration of Japanese government bond (JGB) holdings in the BOJ’s balance sheet, the central bank found it challenging to meet the monetary base target. There were also concerns among institutional investors about the rising scarcity of JGBs, reduced liquidity and functioning of the JGB market, and a negative 10-year yield (Shirai 2020).

Perhaps this is why the BOJ launched a new strategy, known as YCC, in September 2016. The BOJ’s YCC comprises three aspects. First, the monetary base was substituted with two pinpoint interest rate targets: –0.1% (applicable to part of the outstanding balance of the current account of the BOJ) and a 10-year yield set at around 0%. Second, QQE with YCC will continue as long as necessary to achieve the 2% target in a stable manner. Third, the BOJ introduced an inflation-overshooting commitment, where the monetary base will expand until core inflation exceeds 2% and stays above 2% in a stable manner. The BOJ held an implicit tolerance of +/– 10 basis points for the deviation of 10-year JGB yields from its target of 0%. In July 2018, the tolerance band was explicitly expanded to +/– 20 basis points to accommodate market volatility and further to +/– 25 basis points in March 2021.

The COVID-19 pandemic and the yen’s sharp depreciation

Advanced economies took unprecedented monetary and fiscal measures to mitigate the adverse economic effects of the coronavirus disease (COVID-19) pandemic. The BOJ’s reaction was rather muted in terms of asset purchases. Instead, it launched new one-year lending programs at 0% aimed to foster banks’ credit extensions to the domestic private sector while maintaining YCC. To promote banks’ borrowing from the BOJ, the pool of eligible collateral was expanded. The interest rate applied to the BOJ’s outstanding current account balances corresponding to the outstanding amounts of these loans was also raised to 0.1% or 0.2% to mitigate the adverse impacts of the negative interest rate policy and promote banks’ lending. This facility was terminated in March 2023.

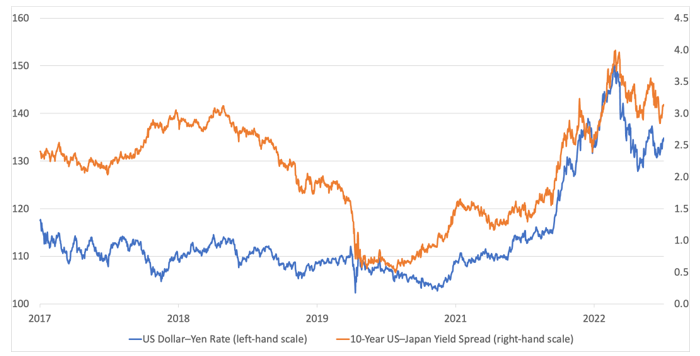

The YCC framework managed to keep the yen’s exchange rate against the US dollar range-bound (in a range from ¥105 to ¥115) for more than 5 years. This changed in 2022, when almost all central banks worldwide started to tighten their policies to cope with rising inflation. The BOJ was the only noticeable exception among developed economies. This interest rate divergence, supported by the YCC, was strong enough to generate substantial yen depreciation (Figure 1). The yen exceeded ¥150 against the US dollar briefly in October 2022 and has since reversed to around ¥130–¥140 with substantial fluctuations, mainly reflecting the decline in the 10-year yield in the United States and speculations over the two central banks’ monetary policy stances. The yen’s depreciation contributed to import inflation and led to the Ministry of Finance’s intervention in the foreign exchange market in September and October 2022.

Figure 1: US Dollar–Yen Rate and the 10-Year Yield Spread between US and Japanese Government Bonds

Source: Prepared by the author based on Bloomberg data.

Source: Prepared by the author based on Bloomberg data.

In December 2022, the BOJ expanded its tolerance band around the 10-year yield target to +/– 50 basis points. This surprise move created substantial volatility in the JGB bond market, mainly because of the denial of such a policy by the BOJ in September 2022. While the earlier expansions of the tolerance band aimed at increasing fluctuations of the yield and can be viewed as steps toward normalization of the YCC, the 2022 decision was conducted for different reasons—namely, to correct distortions and improve the functioning of the bond market.

Conclusions

The BOJ’s holdings of JGBs account for more than 50% of the total outstanding. Given that the ratio of Japan’s public debt to gross domestic product exceeds 260%, the BOJ’s holdings are substantially large. While other central banks have already launched a reversal process, the BOJ remains committed to the YCC, including JGB purchases. As a result, its large holdings continue to exert a substantial impact on the functioning of the bond market. Market participants also focus on risks stemming from the BOJ’s balance sheet from its ownership of diverse financial assets.

Japan’s economy has not yet reached a situation where the price stability target of 2% can be sustained, i.e., accompanied by domestic demand and wage increases (Kuroda 2022). At his final press conference held on 7 April 2023 as governor, Kuroda repeated that a gradual growth in wages is now taking place, and the long-embedded perception in society that it is natural that prices and wages do not rise (the so-called “norm”) appears to be changing. Kuroda also emphasized that unconventional monetary easing had been effective enough to take Japan out of deflation and that the 2% target was not achieved due to the prevalence of the “norm.”

It is not yet clear whether firms will keep raising wages sustainably in the future. It is also yet to be seen how the policies pursued by the BOJ in the recent decade will be evaluated in the future. Kuroda’s legacy depends on how the BOJ led by Kazuo Ueda will treat his predecessor’s policy. On this front, it is important to see a broad-perspective review of monetary policy covering a period of 25 years, which the new BOJ policy board promised at its first April monetary policy meeting to conduct within 1 to 1.5 years.

References

Kowalewski, P., and S. Shirai. 2023. History of Bank of Japan’s More Than Two Decades of Unconventional Monetary Easing with Special Emphasis on the Frameworks Pursued in the Last 10 Years. ADBI Working Paper 1380. Tokyo: ADBI.

Kuroda, H. 2022. Toward Achieving the Price Stability Target in a Sustainable and Stable Manner Accompanied by Wage Increases. Speech at the Meeting of Councillors of Keidanren (Japan Business Federation), Tokyo, 26 December.

New York Times. 2023. Japan Initiates Bold Bid to End Years of Tumbling Prices, 4 April.

Shirai, S. 2018. Mission Incomplete: Reflating Japan’s Economy (second edition). Tokyo: ADBI.

Shirai, S. 2020. Growing Central Bank Challenges in the World and Japan: Low Inflation, Monetary Policy, and Digital Currency. Tokyo: ADBI.