The disclosure of climate-related information by publicly listed companies is gaining global importance. It enables companies to demonstrate their commitment to achieving net-zero greenhouse gas (GHG) emissions through their production and operational activities, with emphasis on the measurement of GHG emissions. Before setting emission reduction targets, companies should start by collecting data and measuring emissions at each stage of their production process, as emphasized during discussions on GHG accounting as part of the ADBI-ADB Climate Dialogue earlier this year.

Why Are GHG Emissions Data Important?

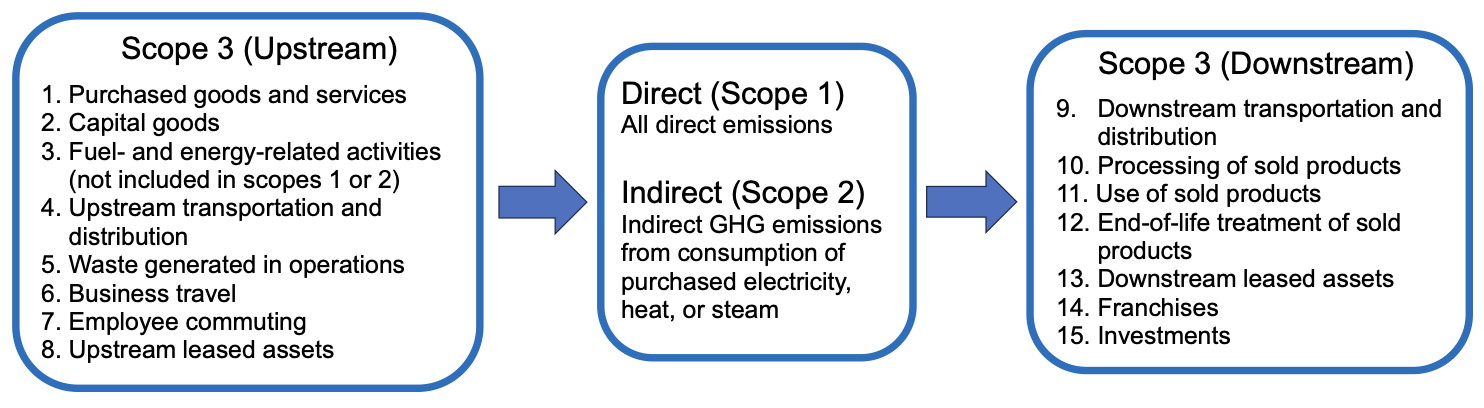

The international standard for GHG disclosure is the GHG Protocol, which classifies GHG emissions into three categories of scope. Companies are expected to disclose emissions as Scope 1 (emissions directly generated by operational activities), Scope 2 (indirect emissions resulting from purchased electricity consumption), or Scope 3 (emissions throughout the entire process from upstream to downstream), as shown in Figure 1. This classification prevents companies from appearing to reduce their own emissions by outsourcing these activities, since Scope 3 includes outsourced activities. Scope 3 emissions often dominate a company’s total GHG emissions, accounting for 70% of the total (CDP 2020).

Figure 1: Measuring GHG Emissions

Source: Shirai and Dang (2024).

Even if only large companies become subject to mandatory disclosure requirements, data from small and medium-sized enterprises will still be necessary for calculating Scope 3 emissions. Additionally, for disclosures by banks, data on financing and investment activities recorded in the 15th category of Scope 3 are required. Therefore, smaller companies should be aware that there are likely to be requests for such data from their large client companies or banks. Some protocol users may be concerned that such practices could result in the double-counting of GHG emissions by companies and lead to an overestimation of total emissions. However, fundamentally, the calculation of emissions is not viewed as problematic because the purpose of the GHG Protocol is to understand how each company is subject to climate change transition risks across its value chain.

Challenges to Measuring Scope 3 GHG Emissions

Ideally, companies should directly measure their emissions using measurement devices and sensors at their facilities. If such primary data are unavailable, companies can collect their own activity data (e.g., production volumes) and use emission factors (emissions per unit of activity) obtained from a third party (secondary data) to calculate their emissions. Detailed emission factor data are available for the United States, the United Kingdom, and Japan, as well as from the United Nations, the Institute for Global Environmental Strategies, and the International Energy Agency.

For Scope 1 emissions from fuel combustion, emissions can be calculated by multiplying the purchased quantities of fuel by the emission factors. For Scope 2 emissions, electricity consumption data at various company locations can be obtained from each electric utility’s contract terms. This “market-based” approach is preferred to the “location-based” approach, which calculates emissions by multiplying the annual electricity consumption of each country by the average emission factor for electricity use in that country.

Calculating Scope 3 emissions poses major challenges because there are 15 categories, and large companies deal with numerous suppliers, whose information is often beyond the companies’ control. The best practice is to obtain emission data directly from major suppliers. If a supplier has calculated its total GHG emissions, a company can calculate Scope 3 data using the ratio of a supplier’s sales to the company. Alternatively, many companies resort to calculating emissions by multiplying activity data by emission factors, and it is preferable to use detailed emission factors per activity for Scope 3 calculations. For categories where obtaining such data is difficult, emission coefficients are provided based on values or prices instead of per activity. In this case, companies calculate the emissions by multiplying the purchase amount from a supplier. The problem with this method is that during inflationary periods when purchase values may soar, there is a risk of overestimating emissions due to inflated values. There is significant variability in the quality of the Scope 3 data because different assumptions and estimation formulas are used. To enhance trust from investors and trading partners, companies should receive assurance from independent third parties with regard to emissions data.

Promoting GHG Accounting and Reporting in Asia

In Asia, the majority of GHG estimates rely on default emission factors from the United Nations or other countries. Using emission factors with default values that do not reflect country conditions is a main source of uncertainty and inaccuracy both at the national and firm levels. In calculating the emissions using emission factors, the Intergovernmental Panel on Climate Change (IPCC) system has three tiers (IPCC 2006): Tier 1 (basic method), Tier 2 (intermediate method), and Tier 3 (most demanding, complex method).

- Tier 1 estimations incorporate default emission factor data, relying on fundamental approaches, and employ standard emission factors using national, regional, or international data.

- Tier 2 estimations provide country- or region-specific emission factors with more localized data. The data are derived using country-specific emission variables. The Tier 2 estimates provide lower uncertainty than Tier 1 estimates, although both use an average emission factor for the source category.

- Tier 3 estimates cover more detailed, specific data derived from intricate emission models or direct measurements of emissions. The Tier 3 emission factor also considers the technology type.

Some Asian countries, such as the People’s Republic of China, India, Malaysia, and Singapore, have made it a priority to develop country-specific emission factors. Singapore and Malaysia are the two most advanced countries in Southeast Asia in terms of developing and applying emission factors utilizing Tier 2 and Tier 3 techniques for several important sectors. Other Asian economies that are in the early stages of development and construction of these data primarily use the United Nations reference dataset for key industrial categories.

The Way Forward

The quantification of GHG emissions data serves as a foundation for investors to evaluate companies’ ability to manage climate transition risks. Emission factors are essentially conversion metrics that enable businesses to translate various operational activities into equivalent GHG emissions. Creating country-specific emission factors that are customized to the unique environment and business conditions of each country is an effective way to tackle a major problem that local businesses encounter. Currently, many Asian companies remain dependent on overseas sources. Support from the international community is crucial for enhancing the ability of policy makers to develop national emission factors.

Learn more about the ADBI-ADB Asian Climate Finance Dialogue.

Read the Key Takeaways from the Second Roundtable of the ADBI-ADB Asian Climate Finance Dialogue.

Read the Key Takeaways and Summary from the Capacity Building Workshop on Corporate Climate Disclosure.

References

CDP. 2022. CDP Technical Note: Relevance of Scope 3 Categories by Sector, CDP Climate Change Questionnaire.

Intergovernmental Panel on Climate Change (IPCC). 2006. 2006 IPCC Guidelines for National Greenhouse Gas Inventories. Volume 2 Energy.

Shirai, S., and L. N. Dang. 2024. Promoting Global Greenhouse Gas Accounting to Drive Corporate Climate Actions and Asian Practices, ADBI Policy Brief No. 2024-10 (June). ADBI.