If the United States Federal Reserve tightens or eases monetary conditions, this impacts emerging economies. Over the years since the global financial crisis, a second type of spillover has emerged: spillovers stemming from the uncertainty about future monetary policy. Uncertainty spillovers exist above and beyond those stemming from specific policy steps. It is the uncertainty about the likely course of monetary policy that led investors to adjust their portfolios, thus leading to side effects on emerging markets. This uncertainty channel of international policy transmission has been highlighted by the financial press. The Financial Times not only recently titled the abovementioned statement, but also stated that “[e]merging markets call on Fed to lift rates and end uncertainty” (9 September 2015) and “Fed clarity on rates is the catalyst that uncertain markets need” (12 October 2015).

The uncertainty about future monetary policy was particularly elevated during the summer of 2013. Fed Chair Ben Bernanke’s testimony on 22 May 2013 triggered an episode of unusual volatility when he reflected about the possibility of exiting quantitative easing (QE) and starting the gradual normalization of monetary policy. Markets reacted with high uncertainty, a rise in volatility, and a sharp increase in US bond yields. This period is known as the “taper tantrum.” The strong market reaction also affected emerging market economies, which experienced strong depreciation of domestic currencies and a sudden tightening of monetary conditions.

Policy uncertainty on Twitter

The key contribution of Tillmann (2016) is a novel dataset, which allows an empirical analysis of the taper tantrum: the dataset consists of 90,000 tweets (Twitter messages), which reflect the entire discussion on the Fed tapering between April and October 2013 on Twitter.com. From this, we construct an indicator of uncertainty about future monetary policy, which we then feed into a standard vector autoregressive (VAR) model. We use a comprehensive word list from the literature which contains key words that describe uncertainty and apply this to all our tweets. This gives us an index of uncertainty which is directed to a very specific monetary policy decision. This is an important advantage over uncertainty indicators used in the literature, which often reflect a broad, unspecific notion of uncertainty. A second advantage is that we measure uncertainty directly from messages sent, read, and forwarded by market participants. A third advantage is that this index is available on a daily frequency.

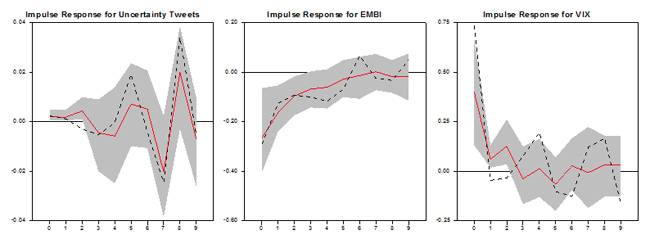

Tillmann (2016) finds that an increase of uncertainty about the timing of the exit from QE leads to significant effects on emerging market economies. The figure below shows the responses of the number of uncertainty-tweets, emerging market bond prices as measured by the Emerging Markets Bond Index (EMBI), and the index of implied volatility (VIX) to an identified uncertainty shock. A shock leads to a significant fall in bond prices and a strong increase in volatility.

Response of EMBI to Uncertainty Shock

EMBI = Emerging Markets Bond Index, VIX = volatility index.

Notes: The shaded area reflects 68% confidence bands. The red line is the median of all draws, the dotted line is the draw that is closest to the median.

Source: Tillmann (2016).

Implications

The taper tantrum period resembles the recent debate about the increases of the federal funds rate target after 9 years of near-zero policy rates: the tapering decision was expected at the June or July 2013 Federal Open Market Committee meeting, then postponed to September 2013, and finally delayed until early 2014. Both the timing and the delays are similar to the “liftoff” of the federal funds rate in 2015, causing observers to refer to a reappearance of the taper tantrum.

The results show the effects of shifts in expectations about future policy and their spillovers to emerging economies. They highlight the need for clear and consistent communication of major policy decisions of central banks in advanced economies. Major policy turnarounds such as the exit from QE should be designed with special attention to the vulnerabilities of emerging economies. This is particularly relevant for, among others, the European Central Bank and the Bank of Japan, which will have to communicate the exit from unconventional monetary policy at some point in the future. Providing a clear path for monetary policy during the exit will help prevent painful side effects for emerging markets. Our results also suggest that maintaining strong macroeconomic fundamentals in emerging markets is best suited to withstand uncertainty spillovers.

_____

References:

P. Tillmann. 2016, forthcoming. Uncertainty about Federal Reserve Policy and Its Transmission to Emerging Economies: Evidence from Twitter.

Photo: By 401(K) 2012 [CC BY-SA 2.0], via Wikimedia Commons

{kind=link}

Comments are closed.