Over 31 million consumers in Viet Nam researched or purchased a product online in 2015. Just ten years ago, internet connectivity was only starting to become common. Digitization is changing how people trade. There are even more dramatic changes happening under the hood. The way trade is financed, processed and regulated has entered a period of disruption. We take this opportunity to consider the short and long term implications of digitization of the trade process. They’re not what you’d expect.

Loosening infrastructure constraints

Digitization and related technologies have already improved development outcomes, even where existing infrastructure appeared to be a binding constraint. For instance, biometric IDs enable 1.009 million Indians to access social services. The number of digital finance users in Asia doubled from 2011 to 2014, despite bank density remaining below the global average.

Simplifying documentation

Trade is a document-intensive process, which slows processing time. Digitization is simplifying the workflow, pushing down costs and reducing risk. Replacing physical documents with electronic versions streamlines time-consuming activities related to the physical movement, recoding and storing of documentation. This also increases accuracy, reduces documentary risk and the likelihood of disputes between parties.

Transparency in risk analysis

Financing trade requires credit and risk analysis, and it is in this step where the disengagement of small and medium-sized enterprises (SMEs) often occurs. SME financial records and collateral are often insufficient, so to assess risk financial institutions must perform more in-depth, and therefore more costly, due diligence on SMEs borrowing small amounts compared with larger firms borrowing much larger amounts.

One novel way to address this problem is an open public online trading system that companies and financial institutions could use to settle transactions. It would enable lenders to see the verified history of a firm’s transactions, including credit history, commercial disputes, and performance risk along the entire supply chain. Such a system would generate the records that SMEs struggle to maintain, and the verified set of transactions would enable banks to assess SME lending risk in a cost effective way. Several consortia of banks are already piloting projects to work through the technical issues. As this goes forward, there is a need for leadership to ensure interoperability.

Standard legal identities

To fully take advantage of online trading systems, SMEs should use a standardized identification number. This is already in progress, and the use of legal entity identifiers (LEIs) has been expanding globally to 448,354 today. A standardized identifier directly reduces the cost of conducting due diligence, and facilitates the collection and tracking of credit, performance and commercial dispute data. The importance of legal identification has already been recognized in the Sustainable Development Goals (SDGs), as SDG 16.9 aims to provide every person on the planet with a legal identity by 2030. LEIs extend the concept to firms.

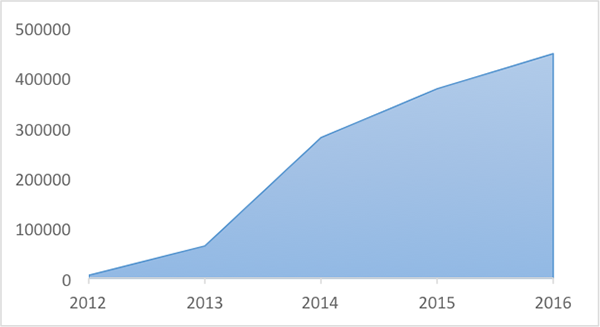

Total LEIs issued globally. Source: Global LEI Foundation. Note: measure is total LEI as of June of each year.

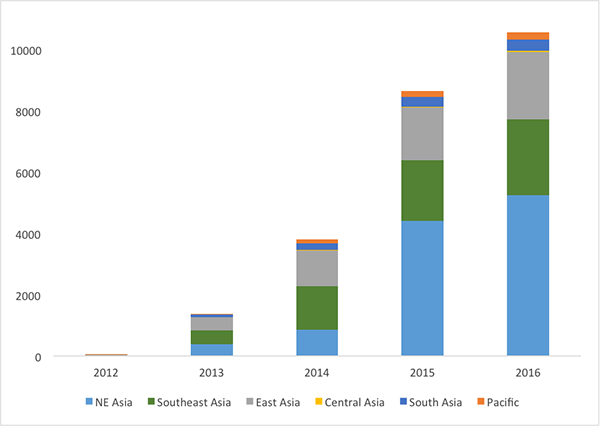

Total LEIs issued in Asia and the Pacific. Source: Global LEI Foundation. Note: measure is total LEI as of June of each year.

Speeding up the supply chain by modernizing the legal process

The processing of trade is slowed down at multiple stages in the supply chain by an analog legal process. Legal processes could be moved into hyper drive by using smart contracts, which encode and execute the workflow associated with a traditional contract. The contracts are self-executing using ‘if-then’ commands. For example, once an electronic payment is made, the smart contract automatically triggers the associated result, which might be that a shipment is released. Or if a payment is not received on time, a piece of equipment will be remotely decommissioned. As this technology gains ground, it has the potential to increase productivity.

Government-backed e-currency

Cross-border currency settlement is costly. Even though trade is typically processed through an electronic payments system, it is backed by physical money in a central bank, which needs to be verified to avoid counterfeiting and double counting. The current payments system is inefficient, prone to errors, expensive and is therefore ripe for disruption. As consumers all over the world have moved away from cash, central banks are also exploring the potential of issuing electronic currency. The idea is that e-currency would function not as a replacement to physical money, but as an addition to it.

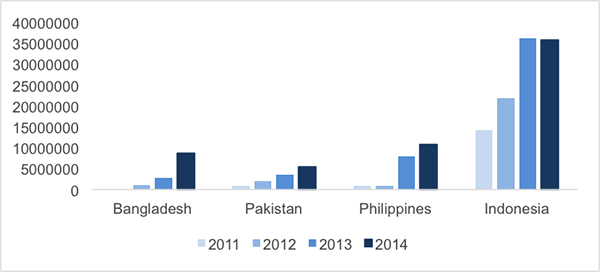

Mobile money accounts (total registered). Source: IMF Financial Access Survey 2015.

Before they launch e-currencies, central banks must consider factors such as implementation details, the capacity of commercial banks to manage the product, and the impact on the financial services industry. However, the trend is inevitable. The Bank of England is exploring its options and both the People’s Bank of China and the Bank of Canada have publicly stated their intention to issue e-currency, although this may be a few years away.

Skepticism around the possibility of creating public open trading windows, smart contracts, government-issued e-currency is understandable given the technical, legal, and regulatory challenges. Yet banks, technology firms and governments have already made significant progress in this areas. The next step is to coordinate various groups involved in trade – bankers, regulators, legislators and companies to agree a compelling vision of the future.

This article was first published by ADB Development Blog.