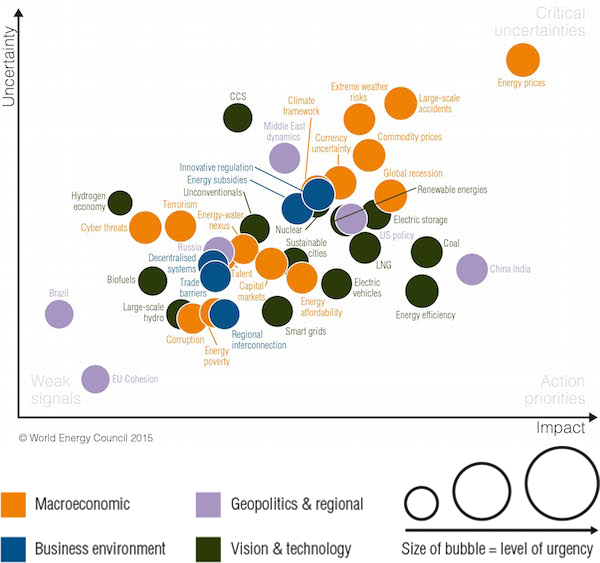

As we gather this week for the 2015 Asian Clean Energy Forum, the context for our meeting has changed greatly from that of last year. We have seen a dramatic drop in the price of oil, which has sent shockwaves through the entire energy sector. Volatility is the new normal, and, for a sector known for its conservative outlook, this drives those at the forefront of the energy challenge to re-evaluate traditional norms. However, we see that it is not just price shocks that keep energy leaders awake at night: extreme weather and large-scale accidents/disruptions top the list of issues facing energy leaders in Asia.

For many years now in our annual World Energy Issues Monitor we have seen that one of the highest critical uncertainties amongst leaders has been the lack of a clear climate framework. While this issue is not the number one high impact-high uncertainty issue in Asia, it is still a key issue across the world. This impacts investment decisions as political risk is kept high and financing models are challenged. This is one of the reasons that 2015 will be an important year for the energy sector, with the much anticipated climate agreement to be hammered out in Paris in December.

Encouragingly we have seen the emergence of new and potentially disruptive technologies coming to market, although it is still to be seen if these will be truly transformational or just another step forward. We have also seen technologies, such as carbon capture and storage (CCS), which are seen by many to be crucial, falling behind in the assessment of energy leaders. This could have significant consequences for our ability to even come close to the 2O temperature rise target set by governments. As our World Energy Scenarios highlights, on current trends, fossil fuels could still represent between 77% (in the Jazz world) and 59% (in the Symphony world) of the global energy mix in 2050, therefore CCS technologies will be critical for mitigation. These scenarios do not seek to set out a roadmap for the future but represent bottom up analysis, based on known and expected technology and policy developments, to produce a more consumer-driven “Jazz” scenario and a more voter-driven “Symphony” scenario, which we believe provide for a more realistic outlook to base decisions.

We see that the global hydroelectric power market, which already represents 76% of all renewable energy globally, has the potential to double to a 2,000 GW capacity by 2050. The total installed capacity has grown by 27% since 2004, which represents an average growth rate of 3% per year. The rise has been particularly strong in emerging markets such as Asia, where hydropower offers not only clean energy, but also provides water services, energy security, and facilitates regional cooperation and economic development.

Solar photovoltaic (PV) is also making great strides as prices continue to fall. As our colleagues at IRENA have recently highlighted, the solar PV industry is now the largest renewable energy employer worldwide, accounting for 2.5 million jobs. With more that 7.7 million people worldwide now employed in the renewable energy industry, we can see that this is a significant growth area for the energy sector, and gatherings such as the Asian Clean Energy Forum are at the forefront of this momentum.

As the sector begins to come to terms with what all these developments will mean for the future, we have seen some companies responding to the new outlook with bold business strategies, and others preferring to bide their time and wait for the context to be clearer. What is clear is that the energy sector almost unanimously wants, and needs, a clear and predictable climate agreement to be finalized in Paris. While this agreement is only the starting point for an agreement that would come into force in 2020, it provides a degree of direction which enables investment decisions to be made and planned.

It is however clear that without coherent national energy policies, we will not be able to deliver a meaningful climate agreement. So often the negotiations at the Conference of the Parties (COP) focus on the priorities of environment and foreign ministers without the full engagement of the energy sector and its ministries. We have seen the development of the proposed Intended Nationally Determined Contributions track which is welcome but must include the energy sector perspective in each country for this to be truly valuable. Coming from Switzerland, famed for its watchmaking prowess, I like to use the analogy of trying to wind up a clock without a movement behind the beautifully crafted face. Without a strong movement, which represents balanced national energy policies, it does not matter how often your wind the clock – it just won’t work properly.

This is why the World Energy Council recommends that when developing national energy policies, or corporate strategies, leaders should look to address the triple challenge of what we call the “Energy Trilemma”. This represents the need to simultaneously consider energy security, energy equity, and environmental sustainability. To neglect one or more of these areas ultimately leads to political risk and underinvestment in critical energy infrastructure.

To neglect the environment side means that unsustainable levels of local pollution will result in health problems and exacerbate water stress. To neglect the equity side means that too expensive electricity will reduce the ability for the energy poor to benefit from modern energy services and thus contribute to the competitiveness of the economy. Energy security is often the main focus for governments, but to singularly focus on this aspect can result in higher energy prices and or overly heavy environmental burden. Consistently neglecting one of these aspects over a prolonged period of time will typically lock a country into a misbalanced system. The unlocking may cost a lot of money, may take a lot of time, and is likely coming after political change that results from built-up frustration.

The energy world is truly at a tipping point. New market design is called for to ensure stable energy markets with increasing renewable shares; new business models are emerging to take advantage of new technological solutions; and new international policy frameworks are required to maximize the broader opportunities. This is why gatherings such as the Asia Clean Energy Forum and the work of ADB are so important, and why the World Energy Council is proud to support this year’s event.

This article was first published by ADB Development Blog

The article on clean coal technology is what appealed to be the most in the present day scenario for the simple reason that it is one of the conventional forms which is up and running, while other forms of energy-clean/green still are grappling with cost effective issues.

But what matters most is to make the population aware of the energy forms, their sources, projecting right numbers in form of fractions and percentiles so that few years down the line we will be able to see what percentage of the grid has come of a particular form of energy. I believe it is still unclear how to get all the different energy forms on to the grid at this point in time.