Soaring fossil fuel prices since 2021, exacerbated further by the Russian invasion of Ukraine this year, have reminded the world that investment in clean and low-emissions energy projects is needed to achieve net-zero greenhouse gas (GHG) emissions by mid-century.

Investment has been inadequate for many years because of the limited scale of climate policies adopted by advanced economies and emerging and developing economies (EMDEs). While an increase in overdependence on fossil fuels might be inevitable for some time due to a structural shortage of energy, the world needs to accelerate transition strategies for net-zero GHG emissions in the near future and focus on addressing natural stock and biodiversity loss.

Advanced economies need to work together on financing EMDEs. Net capital flows to EMDEs, excluding the People’s Republic of China (PRC), dropped since 2019 as declines in net equity and debt capital inflows were more than offset by the increase in net official development assistance (ODA) inflows. Despite an increase in the absolute amount, the ratio of net ODA to gross national income was just 0.33%, failing to meet the United Nations’ (UN) 0.7% target.

At present, energy consumption in EMDEs, excluding the PRC and India, is relatively low, but energy demand is expected to increase in the future in the process of promoting industrialization and urbanization. EMDEs are set to account for the bulk of GHG emissions growth in the coming decades unless much stronger action is taken to transform their energy systems (IEA 2021). Therefore, an unprecedented increase in clean energy investment is required to put these countries on the pathway toward net-zero emissions in a cost-effective way.

How to mobilize private capital to promote climate finance

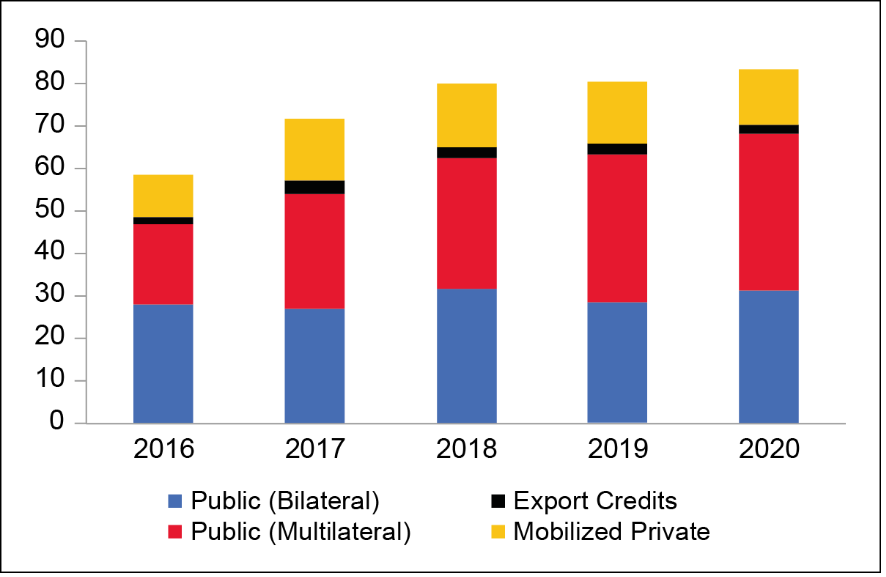

Advanced economies so far have not fulfilled their collective goal of mobilizing $100 billion per year from public and private capital by 2020 and the same amount until 2025—a commitment set at several past United Nations Framework Convention on Climate Change (UNFCCC) Conferences of the Parties (COPs) for EMDEs (Figure 1).

To promote energy transition, advanced economies have created several public-private collaboration initiatives in recent years, such as the Just Energy Transition Partnership in South Africa in 2021 and Indonesia in 2022. However, funding pledges in development finance have been traditionally hard to fulfill, resulting in disparities between commitments and actual disbursements (Liao and Beal 2022). Moreover, it is known that the global environmental finance landscape among donors and multilateral and regional institutions is highly fragmented, leaving accountability for climate finance flows opaque and hard to measure objectively.

Figure 1: Total Climate Finance Provided and Mobilized ($ billion)

Data source: OECD (2022).

Data source: OECD (2022).

Expectations are rising among advanced economies that long-term-oriented institutional investors, particularly investors focusing on environment, social, and governance (ESG), could contribute more funds to achieving net-zero GHG emissions in EMDEs. In light of this, the UN-convened Net Zero Asset Owner Alliance (NZAOA) called asset managers to collaborate in its efforts to increase blended finance vehicles to EMDEs (UN-convened NZAOA 2021). The NZAOA is an initiative of institutional investors committed to transitioning their investment portfolios to net-zero GHG emissions by 2050. Nonetheless, advanced economies should be aware that the role of donor countries and their leadership are essential to mobilize private capital given that ESG investors are subject to financial regulations and fiduciary duties and, thus, are required to take into account returns and risks.

Promoting blended finance with the active use of public funds

The most promising approach is to promote blended finance more extensively to address information asymmetry problems, which tend to be severe in EMDEs (Shirai 2022). ESG investment is rapidly growing in advanced economies, where capital and financial markets are well-developed and numerous issuers and investors are required to disclose audited financial statements. This situation does not necessarily apply to many EMDEs.

A blended finance mechanism, thus, might enable public funds to mainly invest in the initial phase, especially in the form of catalytic funds or equity tranche, and private investors to start financing projects with small amounts. Private investors may provide more funding at a later phase after the project becomes more viable.

Blended finance is important because blending the public fund portion with private funding can attract additional new private funding for projects that otherwise would not have been possible. With the participation of project developers and private companies, as well as experienced multilateral and/or bilateral development finance banks, charitable foundations, and NGOs, etc., blended finance is able to reduce the information asymmetry faced by investors.

Among advanced economies, the European Union has accumulated some experience of blended finance schemes. Given the limited available budgetary resources, advanced economies collectively need to explore how to utilize public funds more effectively in terms of mobilizing more private capital inflows. Donor economies should allocate more funds toward environmentally vulnerable economies, given that less vulnerable economies tend to receive more environmental finance. Traditional public funds tend to include grants, loans, technical assistance, and, to a lesser extent, equity investment.

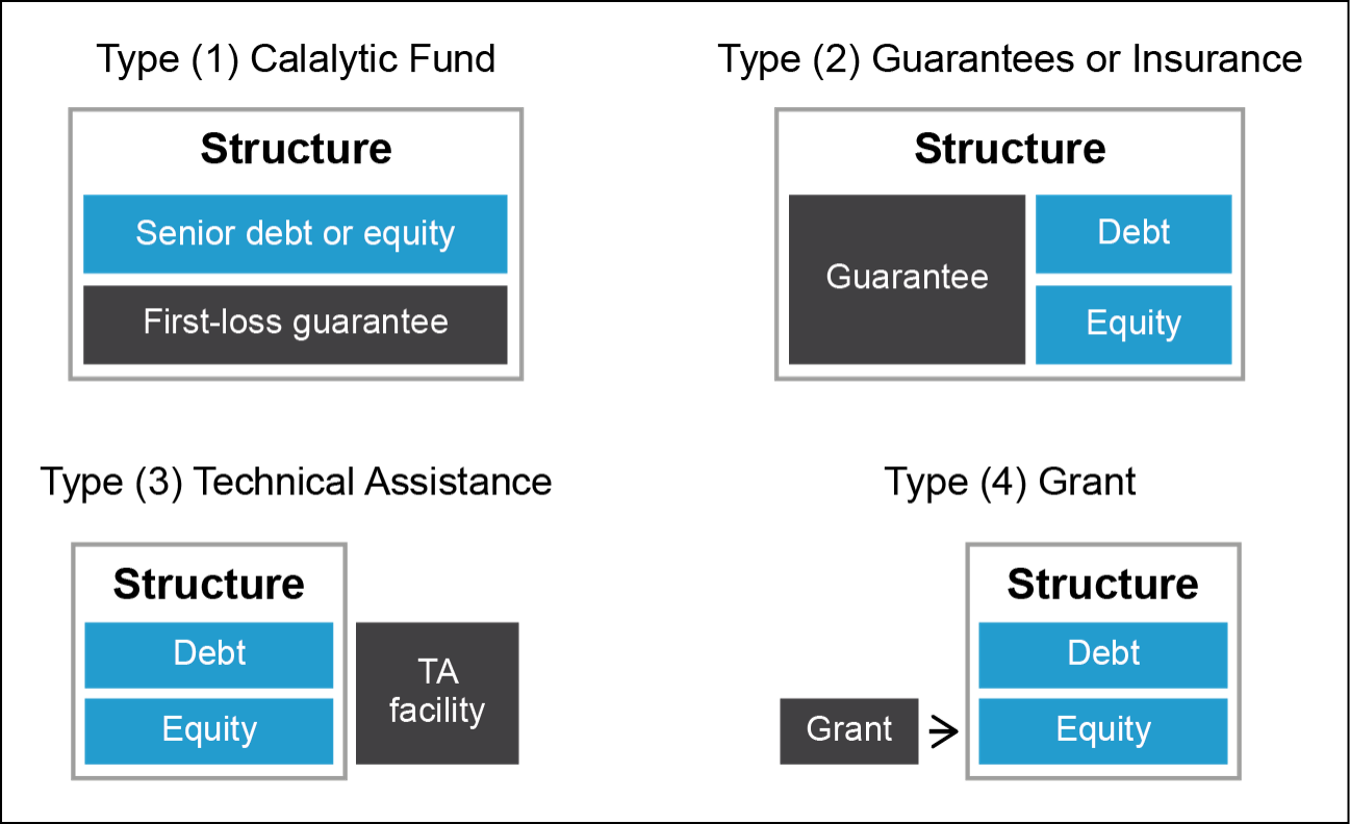

The important role of catalytic funds in blended finance should be discussed by the Group of Seven (G7) and Group of Twenty (G20) to increase collaboration among creditor nations from the perspective of mobilizing private capital (Figure 2). Shifting some grants toward catalytic funds or equity tranche with joint contributions among advanced economies can be also examined.

Figure 2: Four Types of Blended Finance Schemes

Source: Convergence (2021).

Source: Convergence (2021).

In addition, it may be worthwhile to place more priority on increasing the contributions of public and private capital to the specialized multilateral climate and environmental funds that promote blended finance for EMDEs (Shirai 2022). These funds include the UN-led Green Climate Fund and are often intermediated through multilateral development banks or bilateral development institutions, which are able to promote climate projects and institutional investors by forming catalytic funds in a transparent and efficient manner.

More global efforts should be pursued to deepen understanding of various global standards and indicators, including the Blue Dot Network being applied to infrastructure projects, and making them more operational and more widely adopted at the global level at the G20. Some convergence with regard to these environmental and social standards could help lower the burden borne by low-income developing economies. Increased participation from all creditor economies and deeper understanding from EMDEs will be instrumental in generating alignment in development finance and achieving greater positive outcomes.

References

Convergence. 2021. The State of Blended Finance 2021. October.

International Energy Agency (IEA). 2021. Financing Clean Energy Transitions in Emerging and Developing Economies. Paris: IEA.

Liao, C. (Liang), and T. Beal. 2022. The Role of the G7 in Mobilizing for Global Recovery. Chatham House Research Paper, June.

Organisation for Economic Co-operation and Development (OECD). 2022. Climate Finance Provided and Mobilised by Developed Countries in 2016–2020: Insights from Disaggregated Analysis. September. Paris: OECD Publishing.

Shirai, S. 2022. An Overview on Climate Change, Environment, and Innovative Finance in Emerging and Developing Economies. ADBI Working Paper 1347. Tokyo: Asian Development Bank Institute.

UN-Convened Net-Zero Asset Owner Alliance (NZAOA). 2021. Alliance Climate Blended Finance Vehicles’ Call to Action to Asset Managers. NZAOA.