With the center of global economic activity shifting rapidly from the United States and Europe toward Asia, opportunities are being generated for the Pacific developing member countries (DMCs) of the Asian Development Bank (ADB) to benefit from increasing economic interdependence with Asia. Economic transmission channels are (i) trade in goods; (ii) trade in services, in particular tourism; (iii) finance and foreign direct investment; (iv) labor and remittance flows; and (v) aid.

Diverse economic growth

Given the varied economic performance and the varied nature and potential for Pacific DMC economies to benefit from Asian transmission channels, implications are assessed according to three broad groupings of Pacific economies. These groupings accord with the economic growth experiences in the Pacific DMCs as described in ADB’s Pacific Approach 2010–2014 (ADB 2009).

Group 1—the Cook Islands, Fiji, Samoa, Tonga, and Vanuatu—has exhibited some capacity for self-sustained growth. Group 2—Papua New Guinea (PNG), Solomon Islands, and Timor-Leste—are resource-rich economies that have benefitted from the recent boom in demand for raw materials from Asia, but little in the way of structural transformation has resulted. Group 3—Kiribati, the Marshall Islands (RMI), the Federated States of Micronesia (FSM), Nauru, Palau, and Tuvalu—comprises microstates that have little in the way of natural resources aside from tuna fishing and are heavily dependent on aid.

Most Pacific DMCs have experienced poor long-term growth trends, ranging from a real gross domestic product (GDP) per capita average annual growth over the period 2000–2012 of 0% in the case of Kiribati to 1.9% for Palau. These low growth rates arise from many factors, but three in particular affect most of them: (i) their small domestic markets and remoteness from major markets, which results in high costs when participating in international markets; (ii) their undiversified economies; and (iii) the frequent natural disasters experienced. These disadvantages have been compounded by weak and evolving politics, poor policies, and undeveloped institutions.

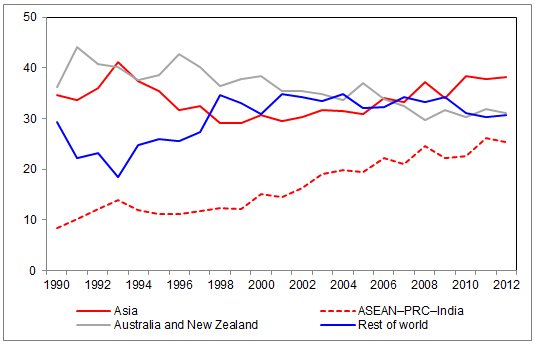

Trade

The volumes and value of Pacific DMC trade are increasing and an increasing proportion of that trade is with countries in Asia (see figure). The distribution of this trade is concentrated in the larger, groups 1 and 2 of Pacific countries such as PNG and to a lesser extent Fiji. Pacific DMC trade with the Association of Southeast Asian Nations (ASEAN) member states and with the People’s Republic of China (PRC) and India has increased noticeably in recent years, with Asian trade with Fiji, PNG, Solomon Islands, and Vanuatu of particular importance. A few commodities, largely primary resources, dominate Pacific DMC exports.

Pacific Trade Shares, by Partner (% of total trade with the world)

ASEAN = Association of Southeast Asian Nations, PRC = People’s Republic of China.

Source: ADB. Asia Regional Integration Center Integration Indicators. http://aric.adb.org/integrationindicators.

For most Pacific DMCs, import values are several times larger than export values. The majority of these economies earn relatively little foreign exchange. They have little domestic processing and even less elaborate manufacturing; therefore, much of what they consume is imported. This structural trade deficit is largely funded by aid. The economies in which imports are not several times larger than exports are Fiji, Nauru, PNG, and Solomon Islands. Again, exports from these island economies are very heavily concentrated in primary commodities.

The tourism industry is of particular importance to Group 1 countries and to Palau. The number of Asian tourists to the Pacific is increasing but this is only important in Palau and to a lesser extent in Fiji. Japan and Taipei,China each account for about one-third of tourists to Palau, with the Republic of Korea comprising 16% of tourists in 2012. Australia and New Zealand remain the major sources of tourists for the South Pacific economies. Both countries account for 60%–70% of tourists going to the Cook Islands, Fiji, Samoa, Tonga, and Vanuatu (all Group 1 countries). However, flights connecting the South Pacific to Asia have begun and the travel industry is predicting a larger presence of Chinese tourists in the Pacific DMCs within a decade or two (Crocombe 2007).

The Pacific DMCs’ trade in certain services is also moving from the United States and Australasia to Asia. This includes shipping, aviation, aircraft and ship repair, as well as medical services. Road, civil engineering, and other construction contracts have also tended to move from Australian and New Zealand firms to those of Asia.

Fishing licence revenues are very important in Kiribati, Tuvalu, and the FSM. Garment manufacture in Fiji and Palau and the manufacture of automotive parts in Samoa are the outcome of trade preferences. However, these industries have been declining as the trade preferences have declined.

The private sector environments in all Pacific DMCs are not overly welcoming to foreign investment, leaving foreign direct investment (FDI) largely attracted to short-term investment, including resource extraction and construction, and to take advantage of preferential trade agreements. Several Pacific DMCs have entered into bilateral investment treaties with other countries to encourage investment flows and to protect investments in each other’s territories. Unfortunately, some Pacific DMC governments have also provided extensive concessions to some of these investors, resulting in little domestic economic benefit. FDI in the Pacific is relatively low, fluctuates greatly, and is mostly concentrated in Group 2 countries and also in Fiji and Vanuatu. There are many instances of sizable (for the Pacific DMCs) FDI from Asia with the promise of much more to come. Outside of Pacific DMC trust fund investments in Asian markets, reciprocal Pacific DMC island investments in Asia have been limited.

Labor migration and aid

One of the most important issues for many Pacific islanders is emigration for work and the opportunity to send remittances back to families. Remittance earnings are significant in the Group 1 economies, excluding Vanuatu and the Group 3 economies of Kiribati and Tuvalu. Remittances to Samoa and Tonga account for 20%–25% of their GDP. The number and range of Pacific islanders in Asia remain limited. Labor movement between the Pacific and Asia has mostly been from Asia to the Pacific. However, even relatively small numbers of Asian workers can have a significant presence in the islands.

Aid to many Pacific economies is high by international levels. Annual official development assistance (ODA) to Pacific DMCs is approximately 10% of their combined annual GDP, with ODA from Asia roughly 10% of total annual ODA. ODA from Australia still dominates the Pacific. However, ODA from Asia is increasing, with assistance from Japan and the PRC the most prominent. Compared to the Pacific’s other donors, the PRC’s aid has grown the most. Relative to GDP, ODA from Asia is more significant to Group 3 economies.

Asia’s diplomatic representation in the Pacific DMCs has tended to follow its commercial interests in trade and investment with most missions from Asia in Fiji and PNG. With the exception of representation in the PRC and Taipei,China, the Pacific DMCs’ diplomatic posts in Asia are again largely those of Fiji and PNG.

Conclusion

Asia’s economic growth offers significant opportunities for economic gain in the Pacific DMCs. Allowing for the far smaller scale and undeveloped nature of the Pacific economies, it does not require much Asian trade, tourism, investment, labor movement, and aid to have a large economic impact in the Pacific. In some Pacific DMCs, and in some goods and services, these opportunities have been taken up. However, these instances are limited overall. Greater Pacific DMC gain will require appropriate economic policies and associated institutions being put in place.

Note

1 Palau could also be included in this group, as it has developed a robust tourism industry.

_____

References:

ADB. 2009. ADB’s Pacific Approach 2010–2014. Manila.

Crocombe, R. 2007. The Fourth Wave: Chinese in the Pacific Islands in the Twenty-First Century. CSCSD Occasional Paper No. 1, May. Available at https://chl.anu.edu.au/publications/csds/cscsd_op1_5_chapter_2.pdf

Comments are closed.