Domestic banking crises often originate in the real estate sector. Therefore, one might conclude that mortgage lending is negative for financial stability. However, in normal (noncrisis) periods, mortgage lending may actually contribute to financial stability. This is because mortgage loans have different risk properties from other bank assets such as commercial loans, so having some share of mortgage loans in a bank’s portfolio tends to diversify the risk of that portfolio. Also, because individual mortgage loans are small, they do not contribute much to systemic risk, except in periods of real estate bubbles (IMF 2006).

In addition, increased mortgage lending can be considered a form of financial inclusion, in the sense that a greater number of mortgage loans reflects greater access by households to the formal financial system, which could be positive for financial stability as well as financial development. For example, Morgan and Pontines (2014) find evidence that an increased share of lending to small and medium-sized enterprises can be positive for some measures of financial stability. Increased mortgage lending could operate in a similar way to increase financial stability, providing that the development of housing price bubbles can be avoided.

Financial stability and mortgage lending

In our working paper just published, we estimate the effect of the share of mortgage loans in total loans by individual banks (together with some control variables) on two measures of financial stability—bank Z-score and nonperforming loan (NPL) ratio. We focus on mortgage lending for two reasons: its importance in overall household credit (averaging about 54% of total household credit in major Asian emerging economies, according to IMF [2011]) and the fact that it is the only variable in the Bankscope database on banks that is related to financial inclusion.

We find evidence that an increased ratio of mortgage lending aids financial stability, mainly by lowering the probability of default by financial institutions and reducing the NPL ratio up to a certain point, but excessive concentration in mortgage loans can reduce financial stability. Few studies have examined the relationship between the mortgage lending ratio and financial stability, despite the importance of real estate lending in many financial systems. And even fewer studies have examined this relationship at the bank level.

Evidence from the advanced economies suggests that household loans have lower default rates compared with larger corporate loans. Also, relative to losses from corporate loans, those incurred from household loans tend to be smaller and more predictable. Thus, the risk that individual household loans pose to financial stability is lower compared with that of corporate loans. Moreover, a balanced portfolio of household and corporate loans would increase the risk diversification of bank portfolios (IMF 2006). Of course, housing booms (and subsequent busts), and the associated movements in house prices, can lead to financial crises and economic downturns.

Data and stylized facts

We analyze the effects of the mortgage loan ratio on bank Z-score and the NPL ratio for our sample, which comprises 212 banks in 19 emerging Asian economies.1 The data are annual, and the unbalanced panel sample covers the period 2007–2013. Bank-level data were obtained from the Bankscope database.2 None of the economies in the sample had housing bubbles or financial crises in this period, so the data sample corresponds to a normal (noncrisis) period. The results may differ if crisis periods are included.

The first measure, bank Z-score, is a widely used indicator of financial stability. It is defined as:

(ROA+equity/assets)/sd(ROA),

where ROA is average annual return on year-end assets, assets are total year-end assets, and sd(ROA) is the standard deviation of ROA (World Bank 2013:23). The numerator of the Z-score is the equity already on the balance sheet plus the current year’s profits. A higher Z-score signals a lower probability of bank insolvency, and hence implies greater financial stability.

The second measure is the ratio of NPLs to total loans. Bank NPLs represent future potential capital losses, so a higher NPL ratio implies potentially lower financial stability.

Mortgage loan ratio as a measure of financial development and inclusion

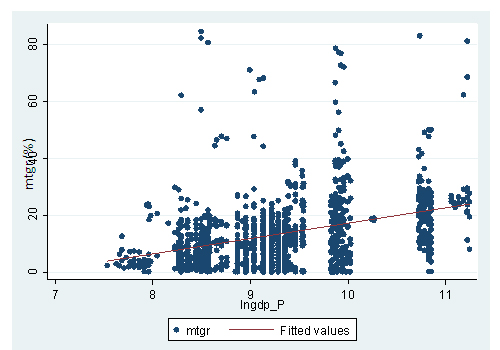

Casual observation shows that, similar to other measures of financial development and inclusion, the mortgage loan ratio increases significantly in line with per capita gross domestic product (GDP) (Figure 1).3 This suggests that the mortgage loan ratio can be considered an indicator of both financial development and financial inclusion.

Figure 1: Mortgage loan ratio versus per capita GDP

GDP = gross domestic product, lngdp_P = per capita GDP in nominal US dollars in log terms, mtgr = mortgage loan ratio.

Sources: World Bank Global Financial Inclusion Database; Bankscope database; authors’ estimates.

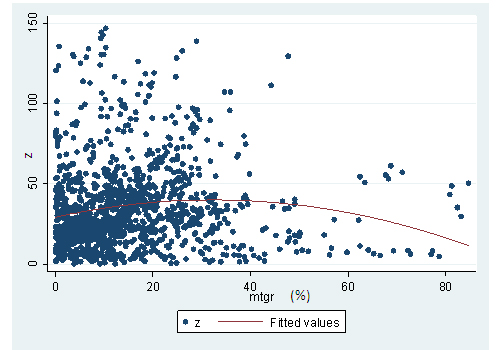

Further, Figure 2 shows evidence of an inverted U-shape relationship between the mortgage loan ratio and the Z-score. For mortgage loan ratios up to about 30%–40%, a rising mortgage loan ratio tends to be associated with higher financial stability. However, above around 40%, the relationship turns negative, suggesting that higher mortgage loan ratios may be negative for financial stability. This is consistent with the expectation that the advantages of asset diversification will diminish if a bank’s loan portfolio is excessively concentrated in mortgage loans. Similarly, we find a U-shaped relationship between the mortgage loan ratio and the NPL ratio, suggesting that a mortgage loan ratio of 30%–40% is consistent with relatively low NPLs, i.e., higher financial stability.

Figure 2: Mortgage loan ratio versus bank Z-score

z = Z-score; mtgr = mortgage loan ratio, simple regression of z on mtgr and mtgr2

Sources: Bankscope database; authors’ estimates.

Results

Regression results for the Z-score and NPL ratio using both ordinary least squares and generalized method of moments confirm the results of a U-shaped relationship with the mortgage loan ratio more rigorously.4 Based on the estimated coefficients, the Z-score reaches its highest predicted value when the mortgage loan ratio lies between 30% and 40%, depending on the equation specification. Similarly, the regression results for the NPL ratio imply a U-shaped relation with the mortgage loan ratio. In both cases, the results imply that increases of the mortgage loan ratio up to 30%–40% improve financial stability, but that higher levels tend to worsen it again. This is consistent with the expectation that a more diversified loan portfolio tends to reduce financial risk, but excessive concentration in mortgage loans (or other loans) tends to increase risk.

Conclusions

The main contribution of our study is to find a relationship between the mortgage loan ratio and measures of financial stability, an area which has been little studied. Also, we find that the mortgage loan ratio tends to rise with per capita GDP, which suggests that it can serve as an indicator of both financial development and financial inclusion.

Up to a critical level of 30%–40% of total loans, an increased mortgage loan ratio is positive for a bank’s financial stability, specifically by lowering the probability of default by financial institutions and reducing the ratio of NPLs. However, if the mortgage loan ratio exceeds that level, the impact on financial stability becomes negative. This result is consistent with the notion that asset diversification increases stability, whereas asset concentration is negative for stability.

Therefore, the challenge is to balance the expected improvement in financial stability due to asset diversification against negative impacts that might result from easier lending standards or too rapid an increase in mortgage lending that could trigger a price bubble in the housing market. This highlights the need for prudent monetary policy and macroprudential policy measures such as loan-to-value ratios to forestall the development of such bubbles.5 Further work in this area is needed.

_____

References:

International Monetary Fund (IMF). 2006. Household Credit Growth in Emerging Market Countries. In Global Financial Stability Report: Market Developments and Issues. Washington, DC: International Monetary Fund. September. pp. 46–73.

———. 2011. Housing Finance and Financial Stability—Back to Basics? In Global Financial Stability Report: Durable Financial Stability: Getting There from Here. Washington, DC: International Monetary Fund. April. pp. 111–157. http://www.imf.org/external/pubs/ft/gfsr/2011/01/pdf/chap3.pdf

Morgan, P., and V. Pontines. 2014. Financial Stability and Financial Inclusion. ADBI Working Paper 488. Tokyo: Asian Development Bank Institute. http://www.adb.org/publications/financial-stability-and-financial-inclusion-0

Morgan, P., P. J. Regis, and N. Salike. 2015. Loan-to-Value Policy as a Macroprudential Tool: The Case of Residential Mortgage Loans in Asia. ADBI Working Paper 528. Tokyo: Asian Development Bank Institute. Available: http://www.adb.org/publications/loan-value-policy-macroprudential-tool-case-residential-mortgage-loans-asia

World Bank. 2013. Global Financial Development Report. Washington, DC: World Bank.

Notes:

- Bangladesh; People’s Republic of China; Hong Kong, China; Indonesia; India; Kyrgyz Republic; Republic of Korea; Kazakhstan; Sri Lanka; Malaysia; Nepal; Philippines; Pakistan; Singapore; Thailand; Tajikistan; Taipei,China; Uzbekistan; and Viet Nam.

- Bureau van Dijk. Bankscope Database. (accessed 15 March 2015).

- Per capita GDP here is shown in nominal US dollar terms, but the picture is very similar for per capita GDP in purchasing power parity (PPP) terms.

- The regression results are described in detail in our paper.

- Morgan, Regis, and Salike (2015) show that loan-to-value ratios can be effective in reducing the growth rate of mortgage loans in a panel of Asian economies.

* The arguments in this post are covered in greater depth in P.J. Morgan and Y. Zhang. 2015. Mortgage Lending and Financial Stability in Asia. ADBI Working Paper 543. Tokyo: Asian Development Bank Institute.

Photo: By Sourav Niyogi (Own work) [GFDL or CC-BY-SA-3.0], via Wikimedia Commons

{kind=link}