Access to energy sources at low prices will continue to drive the world’s political agenda as energy is a component as well as an object of national power. The world’s primary energy consumption from commercial sources of energy has grown from approximately 8,600 million tons oil equivalent (mtoe) to 13,000 mtoe from 1995 to 2015 and is forecasted to grow approximately by the same amount to 17,300 mtoe by 2035.

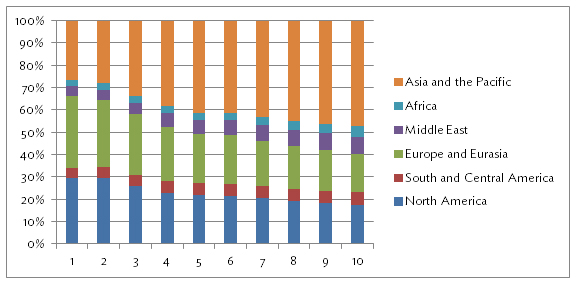

Figure 1: World’s share of commercial energy consumption (1995–2035)

Note: Data are in steps of 5 years, but the latest data (2014) are additionally shown. Data before 2015 are derived from actual statistics, while data after 2014 are based on forecasts.

Source: BP (2016).

A significant change is the decline in the share of total world energy consumption in North America (29.5% to 21.5%) and Europe and Eurasia (32.5% to 22%) from 1995 to 2015 (see figure above). It is counterbalanced by a corresponding increase in energy consumption (26.5% to 41.5%) in Asia-Pacific and this share is forecasted to increase to 47.5% by 2035. This increase is fueled by the growth of energy consumption in the People’s Republic of China (PRC) which is estimated to rise (1.5 times) from 3,000 mtoe in 2015 to 4,400 mtoe in 2035 and emerging economies such as India, where the total commercial energy demand is forecasted to more than double from 660 mtoe to 1,500 mtoe during the same period.

While India would continue to lag significantly behind the PRC and the United States (US) in terms of absolute energy consumption in the next 2 decades, it is important to note that India’s increase in energy demand will be larger than the growth in any of the world’s regions including the PRC. This would make India the fastest-growing energy consumer among Africa, Southeast Asia, Middle East, and Latin America, which would have worldwide geopolitical and economic impacts.

The New Policies Scenario presented in World Energy Outlook 2015 (IEA 2015) forecasts that India’s demand for oil will grow by 6 million barrels per day (mbpd) from 2014 to 2040, surpassing the PRC’s growth in demand of oil (4.9 mbpd) to reach around 9.8 mbpd in 2040. India is expected to become the second-largest oil importer around 2035, overtaking the US, which itself ceded the top spot to the PRC in 2015. A similar story unfolds for coal, with the largest growth in demand in the world during the same period. Although the PRC will lead the demand in growth for natural gas, India’s demand is likely to increase by 100 mtoe during the period. As India has low reserves of crude oil and natural gas, this growing demand has to be met by energy imports, and India is emerging as a major market for energy producing countries.

While the oil and gas market is turning into a buyer’s market due to surplus production and lowering demand from the PRC, India’s negotiating power is increasing by the day. This was evident in the revision of liquefied natural gas (LNG) prices between Petronet (India) and Rasgas (Qatar) wherein the Government of India successfully renegotiated the contracted price from $12–$13 per million British thermal unit (mBtu), which was applicable from 2004 onward, to $6–$7 per mBtu at the end of 2015. While the deal included an increased offtake from 7.5 million tons per year to 8.5 million tons per year, was hailed as a win–win for both parties, it was evident that the decision was in India’s favor. The waiver of a penalty of nearly $18.5 billion on account of low offtake (68% only in 2015) of LNG was an additional benefit. This renegotiation of price opens up avenues for other oil and gas-importing countries to revise their long-term price contracts, which would be accompanied with significant loss of revenues for energy-exporting Gulf countries.

Indian Prime Minister Narendra Modi’s energy diplomacy has also yielded results with the inauguration of work on the long-stalled Turkmenistan–Afghanistan–Pakistan–India (TAPI) pipeline which will bring central Asian energy reserves to the power-hungry economies of India and Pakistan. India will soon start importing crude oil from its erstwhile major supplier Iran after the lifting of economic sanctions. India could well make this payment in rupees, a mechanism which it has successfully tried with Iran earlier (Narula 2014).

India has also ensured the supply of imported nuclear fuel by signing fresh agreements with Kazakhstan for 5,000 metric tons of uranium between 2015 and 2019; Uzbekistan for supply of 2,000 metric tons of triuranium octoxide (U3O8, a compound of uranium) from 2014 to 2018; and Canada for supply of 3,200 tons of U3O8 up to 2020, the first shipment of which arrived in December 2015. India also signed a bilateral safeguard agreement with Australia in September 2014 to enable the supply of nuclear fuel and has ensured continuity of supply of nuclear fuel from the Russian Federation and France. India is the only country which has not signed the Treaty on the Non-Proliferation of Nuclear Weapons but is a recipient of nuclear fuel by the Nuclear Suppliers Group. This has raised India’s profile as a responsible nuclear power and has strengthened its bid to be accepted as a member of the Nuclear Suppliers Group when its application comes up for review in June 2016.

India’s efforts in the renewable energy space have also been credible. Clean energy has figured prominently in India’s talks with the US, the United Kingdom, Germany, France, and a host of other countries with signing of accompanying agreements and/or memorandums of understanding (MoUs). The target of the National Solar Mission has been revised from 20 gigawatts to 100 gigawatts, which would make India the second-largest producer of solar power in the world by 2022. The Make in India and the Skill India programs, which are being aggressively pursued by the government, along with the entrepreneurial spirit of the people of India, will go a long way in making India the renewable energy capital of the world.

India’s role in promoting renewable energy is evident from the launch of the International Solar Alliance at the Paris climate summit in November 2015. The alliance, a cooperative effort of over 120 countries, will channel efforts to commercialize solar power generation by providing finance and technology and endeavors to raise $1 trillion from multilateral institutions and private sources. Its headquarters was inaugurated near New Delhi jointly by French President François Hollande and Prime Minister Modi in January 2016. India’s leadership was also apparent in the Conference of the Parties 21 meeting under the United Nations Framework Convention on Climate Change (UNFCCC) where it showed maturity by leading the developing countries group to agree to contribute to the effort of mitigating emissions in the best interest of developing a robust global climate agreement.

India is clearly moving to the center stage of the world’s energy system. With growth in the PRC slowing down, India’s blip on the energy radar is growing and it is poised to be a major player in the conventional energy market and as a renewable energy producer. On the one hand, India’s rising appetite for energy drives its diplomacy. On the other, its low-carbon growth policies are a commitment to sustainable development. It can thus be concluded that India will continue to influence the global energy agenda for the coming few decades.

_____

References:

BP. 2016. BP Energy Outlook 2016 Edition. London, UK. (accessed 19 March 2016).

International Energy Agency (IEA). 2015. World Energy Outlook 2015. (accessed 25 March 2016).

Narula, K. 2014. Oil Payments to Iran – Advantage India or A Lost Economic Opportunity. (accessed 26 March 2016).

World Nuclear Association. Nuclear Power in India. 2016. (updated 26 February 2016, accessed 29 March 2016).

Photo: By indiawaterportal.org from India (The Kudankulam Nuclear Power Plant (KKNPP)) [CC BY-SA 2.0], via Wikimedia Commons

.jpg){kind=link}