One of the most significant new developments in the global post-global financial crisis (GFC) economy is the enormous asset purchase programs implemented by central banks in the industrial world to stimulate their economies. Widely known as quantitative easing (QE) programs, their impact has been substantial.

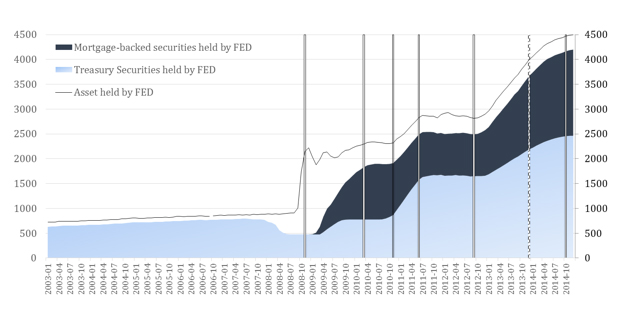

For instance, after three rounds of quantitative easing over a 5-year period, the US Fed’s balance sheet increased more than fivefold from below US$800 billion in 2008 to US$4.4 trillion in 2014 (figure below). The Bank of England purchased £200 billion (US$280 billion) worth of government securities from March 2009 to January 2010, representing around 14% of the annual gross domestic product (GDP) of the United Kingdom. Similarly, in Japan, the central bank has set a target of ¥80 trillion (US$733 billion) in government bond purchases per year from October 2014, about 16% of its GDP. And most recently, the European Central Bank (ECB) has raised its monthly bond purchasing to €80 billion (US$86 billion) after the eurozone launched its QE programs in early 2015.

Compared to traditional interest rate policy, these large-scale asset purchase schemes are the main components of a so-called unconventional monetary policy. Yet, this no longer seems so unconventional. As the examples above show, it has become a fairly common tool that is being widely adopted by the monetary authorities of the industrial world.

Total assets held by the Federal Reserve ($ billion)

Note: The cutting points for the three QE periods and tapering are as follows: QE1 (Nov 2008–Mar 2010), QE2 (Nov 2010–Jun 2011), QE3 (Sep 2012–Dec 2014), and tapering (Dec 2013–Oct 2014).

Source: The figure is constructed using monthly data from Federal Reserve Economic Data (FRED).

Given the fast pace and massive scale of this new development, growing concerns about its effects are being voiced in the developing world, and especially within emerging economies, which are increasingly integrated with the global financial market (Kawai 2015). For Asian policy makers, some important questions requiring answers are:

- Will these immense asset purchases spill over to Asian financial markets?

- What type of spillover effects are to be expected, large or small, and in which sector(s)?

- Will they facilitate a credit boom or relieve the credit shortage in the region?

With these matters in mind, we commenced a study with a focus on the US QE programs and their effects on the loan market in emerging Asia, in particular the syndicated loan market (Xu and La, forthcoming). The syndicated loan market represents a substantial part (approximately 40%) of international banking activities, which could be a major channel for credit spillover.

In response to quantitative easing in the US financial market, we find that dollar credit growth increases in Asia. This emphasizes the importance of credit flows in transmitting financial conditions. Moreover, we find that the overall spillover effect, on average, is large in Asia, irrespective of types of firms, financing purposes, and loan maturity, but that it differs across the stages of QE programs. At the early stage, the spillover exists for non-financial firms but not for financial firms, and for financing real investment but not for debt repayment. However, as the Fed asset programs continued and intensified toward 2013 and 2014, US dollar-denominated credit quickly flowed into financial firms and financial assets.

Our results also show that the early QE programs produce substantially larger increases in loans and do so faster in the short-term segment relative to the medium to long term. Given the fact that loan syndication is typically used to finance large-scale, long-term projects, this raises concern regarding term mismatch.

With the US Fed’s exit from QE programs and the dollar strengthening accordingly, the reversal of dollar credit is expected to increase the rollover costs of those short-term dollar debts or make refinancing impossible. Overall, the debt burden will increase for existing borrowers, and especially for firms that are heavily reliant on dollar credit in the market without having properly hedged the foreign exchange risks.

Our study reveals the unintended consequences of monetary policy spillovers from the US to the Asian credit market. What can policy makers do in response?

Joining Brunnermeier and a group of international experts on cross-border capital flows (2012), we recommend global regulation and globally coordinated monetary policy responses. Proper regulation on cross-border banking requires global regulatory coordination, as multiple stakeholders and not a single authority are involved. Likewise, globally coordinated monetary policy can help reduce the negative externalities. However, while these policy prescriptions are effective in principle, they are challenging to implement in practice because regulation design and monetary policy often prioritize domestic rather than global imperatives.

In the region, we see a number of encouraging initiatives on regional cooperation and safety nets have been put in place, yet concrete actions should follow policy dialogue and information exchange (Kawai 2015). Institutions such as the ASEAN+3 Macroeconomic Research Office and APEC forums as well as regional financial safety nets such as the Chiang Mai Initiative Multilateralization could have an effect, but it will not necessarily be large without a clear policy agenda and binding enforcement mechanisms.

Macroprudential policies may have a straightforward effect by imposing targeted regulations on banks engaged in cross-border activities. In addition to the traditional instruments such as caps on loan-to-value, debt-to-income, and non-core liabilities, countercyclical capital requirements should be carefully designed and properly put into effect. More importantly, constant efforts should be made to monitor and share information on the balance sheet capacity of global banks to adequately manage the potential risks in the cross-border credit market.

The Asian market has become one of the most dynamic financial markets in the world and it is rapidly integrating with the global financial markets. Interdependence has become the key feature of the 21st century global financial landscape where stability and prosperity hinge. We will keep watching this space.

_____

References:

Brunnermeier, M., P.R. Lane, D. Drodrik, J. De Gregorio, J. Pisani-Ferry, K. Rogoff, B. Eichengreen, E. Prasad, H.S. Shin, M. El-Erian, R. Rajan, A. Velasco, A. Fraga, M. Ramos, B.W. Di Mauro, T. Ito, H. Rey, and Y. Yu. 2012. Banks and Cross-Border Capital Flows: Policy Challenges and Regulatory Responses, Committee on International Economic Policy and Reform. Washington, DC: Brookings.

Kawai, M. 2015. International Spillovers of Monetary Policy: US Federal Reserve Quantitative Easing and Bank of Japan’s Quantitative and Qualitative Easing. ADBI Working Paper No. 512. Tokyo: Asian Development Bank Institute.

Xu, Y., and H.A. La. 2016, forthcoming. Spillovers of US Unconventional Monetary Policy to Emerging Asia: The Bank Lending Channel. ADBI Working Paper Series.

Photo: By Dan SmithRdsmith4 (Own workOwn work) [CC BY-SA 2.5], via Wikimedia Commons

{kind=link}