Is fiscal and/or political union, where more sovereignty is shared among countries in Europe’s Economic and Monetary Union, the way forward for the eurozone to stay together and deal with economic and financial divergences among member states? Differences in size, development, and institutions present the monetary union with a policy coordination dilemma, as countries often tend to let domestic interests prevail on agreed commitments. At the current juncture, and learning from the sovereign debt crisis, the countries of Europe need to consider what is the best institutional framework for the monetary union. Such a framework should avoid the building up of imbalances and help countries to live with the euro and within the currency union. Is political union the way forward for EMU? Surely continuing the status quo is not an option.

Is fiscal and/or political union, where more sovereignty is shared among countries in Europe’s Economic and Monetary Union, the way forward for the eurozone to stay together and deal with economic and financial divergences among member states? Differences in size, development, and institutions present the monetary union with a policy coordination dilemma, as countries often tend to let domestic interests prevail on agreed commitments. At the current juncture, and learning from the sovereign debt crisis, the countries of Europe need to consider what is the best institutional framework for the monetary union. Such a framework should avoid the building up of imbalances and help countries to live with the euro and within the currency union. Is political union the way forward for EMU? Surely continuing the status quo is not an option.

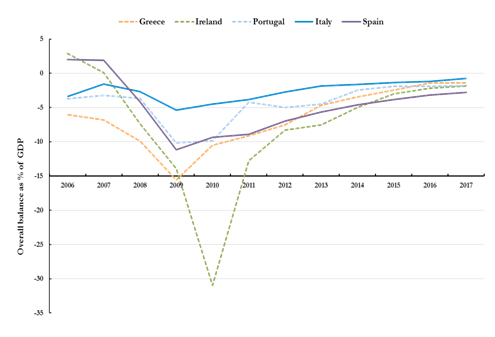

Two years after Greece’s insolvency crisis the political deadlock in Europe has eased, but it remains unresolved. The long-term projection of the deficit countries’ overall fiscal balance as percentage of GDP indicates a convergence toward zero, which means the overall fiscal imbalance could be corrected by 2017 (Figure 1).

Figure 1: Overall balance as a % of GDP

Source: International Monetary Fund Fiscal Monitor, October 2012

This is based on the assumption that crisis countries will manage their fiscal positions – political opposition and social tensions notwithstanding. However, the structural issues embedded in the institutional design as well as in the economics of the single currency have not been tackled. Uncertainties and risks remain. In particular the outcome of the forthcoming election in Italy remains uncertain. A eurozone breakup is possible if long-term steps are not taken.

What started the eurozone crisis?

The eurozone crisis is multifaceted and has its roots in problems that in some countries predated the creation of the monetary union. Long-standing problematic fiscal positions, underperforming economies, and imbalances were the main sources of Europe’s vulnerability to the 2008 global financial crisis and later to the sovereign debt crisis. In addition, unsustainable government borrowing, high unemployment among youth, declining productivity, lack of competitiveness in the eurozone periphery countries, and distressed household finances also contributed to the beginning of the crisis. The eurozone crisis is a multidimensional crisis rather than just a fiscal one.

Is a roadmap necessary?

Europe’s sovereign debt crisis has exposed the deficiencies in the governance of the EMU, shown the limits of its framework of policy cooperation, exposed the imbalances in Europe, exacerbated the structural weaknesses of its model of growth, and emphasized Europe’s regional differences.

Having dealt with the emergency created by the crisis, the eurozone now needs a menu of solutions that includes: short-term measures to restore confidence in countries and support growth; medium-term fiscal measures to reduce deficits and gain credibility with the markets; and long-term structural reforms to support sustainable and balanced growth. Economic competitiveness should be enhanced through reforms that ensure that real exchange rates can adjust with ease. And growth should come before fiscal adjustments, because fiscal adjustments without growth risk backfiring.

Are reforms enough or is a political union the solution?

Because of the close links and interdependence of eurozone economies, the crisis was transmitted through the financial and banking systems. Also, in forming the monetary union, the structure of incentives for countries to join was faulty. The incentives are always present for member states to promote their national interests at the expense of other members of the monetary union. Moreover, weak institutions and problematic political systems in some countries do not guarantee the implementation and respect for the commitments made with other member states in the monetary union.

A long-term solution to the crisis needs to include steps to reconcile national interests with the collective good. First is the need for a banking union, which must be agreed on despite divergent views. Second is the need for implementation of the Fiscal Stability Treaty, which was signed on 2 March 2012 by all member states of the European Union, except the Czech Republic and the United Kingdom. Last, but most important, is the need for a robust political framework which could be, but need not necessarily be, in the form of a political union.

A political union would be difficult but not impossible. It is the way forward to monetary union in Europe for several reasons. In Europe the balance of economic power as measured by GDP is skewed towards Germany, followed by France and Italy. The eurozone lacks leadership, which makes its decision-making process a complex and time-consuming task. So, a well-defined political framework should address the eurozone’s leadership problem and the lack of bargaining power of smaller economies.

Dani Rodrick’s trilemma of the world economy [1] shows that democracy, national sovereignty and deeper economic integration are mutually incompatible because deeper economic integration eventually requires the removal of barriers created and preserved by nation states. Eurozone citizens therefore will eventually need to choose two of these three objectives. If they want to preserve the nation state and democratic politics they will have to accept less integration. But, if they want deeper economic, financial, and monetary integration they will have to surrender some national sovereignty.